When Is the Right Time to Invest? Market Volatility & Timing Explained

One of the most frequently received questions ever at Black Swan Capital, is “Is this a good time to invest or should I wait?”.

It is a sensible question and one that is made more difficult to answer for the typical investor by the sheer scope and of information available, and of course by the poor quality of much of it, including out and out disinformation.

We will address this question and how to navigate the data to make the right decisions for you. We have broken the responses to this question into 4 components below: your objectives, the opportunity cost, your capacity for loss, and the impact of time.

Your Objectives

In all important financial decisions, we are strong believers that the best decision for you should be based on your objectives, what you are trying to achieve. This means that two people could have completely different ‘best courses of action’ at a given point in time.

When you are asking whether it is a good time to invest, follow it up with the questions, ‘what am I trying to achieve?’ and ‘why am I investing?’. A component of your response will include when you want or need to achieve this objective. If the timeframe is particularly short, for example your goal is to have a deposit for a property purchase in 3 months time, it is definitely not a good time to invest, irrespective of the stage of the market cycle. Your primary objective should be accumulation and retention, avoiding short term market movements.

If your objective is to have a deposit for a property in 10 years time, it is a different situation and it might be a good time for you to invest. You might be aiming to maximise growth knowing that time will smooth out short term market movements. See point four on time below.

The key message here is that the answer is specific for you. This is why generalised comments on social media or in the press can not only be unhelpful, they can be harmful. Seek advice that is designed for you. Speak with us at Black Swan Capital.

Opportunity Cost

The second component in our checklist of whether it is a good time to invest for you is the opportunity cost. If you studied economics at school or university, you will recall that every decision carries an opportunity cost. Simply described this is what you cannot do with your money because you used it for the decision you did make.

Trying to time the market often carries an opportunity cost. In part this is because no one knows what the market will do tomorrow. We have seen this repeated many times across our careers. The most repeated scenario is when a person decides to not invest and hold their funds in cash- they are deciding that later will be a better time to invest than now- on the hope that markets may fall in the future and offer a cheaper entry point. There are several ways this can go wrong. First, they may not be right and markets continue on their steady increase in value over time. In this case if markets grow at 6% per annum, and cash at bank returns 1%, the opportunity cost, or amount lost is 5%.

There is a second way where the person is kind of right but not exactly. In this scenario, the markets continue to rise for a year at 6% and then fall 5%. They were right that the markets fell but they grew more than they fell and they would still have been better off investing earlier.

It is very difficult to time a market and when it is done precisely it is more luck than judgement that sees it achieved. Therefore if this is your rationale for not investing, we would recommend to go back to point one, and align your decision to your objectives, but not sit out because a market might ‘correct’.

The insidious impactor of sitting in cash as markets continue to grow is inflation. It was more apparent immediately post Covid when inflation was higher, but even if inflation is 2-3% per annum, if you are not getting more than that in returns you are losing purchasing power and going backwards.

Capacity for Loss

The third criteria in assessment is again personal and specific to each person. It is what we call your ‘capacity for loss’, and our existing clients may recall us speaking with you about this. It is an unusual idea in that no one like the idea of losing money. The reality of investment markets is that they go up over time but not in a straight line. Sometimes they fall. They inevitably recover and will go to new higher levels. That path which goes up, down, and up again is what we call volatility. If you aim to achieve higher growth in the long term, you will have to be willing to take on some of this shorter term volatility.

Your capacity for loss then is what does it mean if your investment does incur a short or medium term down turn, whether you like the idea of it or not. It can relate to your investment time frame, your stage in life, your objectives, and how much of your assets are exposed to this volatility. For some people market volatility could have profound impacts on achieving their financial plans. These investors should adjust their portfolios accordingly. For others, a market downturn might be a minor annoyance, or an irrelevance, and for others it could represent an opportunity.

When addressing the question of whether it is a good time to invest or not, having considered your objectives, you should also think about this idea of what impact a market downturn will have, or as we describe it, your capacity for loss.

Time

Finally, we will expand on time, not in the metaphysical quantum context, that is a bit beyond the scope of this article, not to mention our areas of expertise! We will expand on the consideration and impact of time in this decision making process. We touched on time in the three points above.

When answering whether or not it is a good time to invest, your timeframe will help you decide.

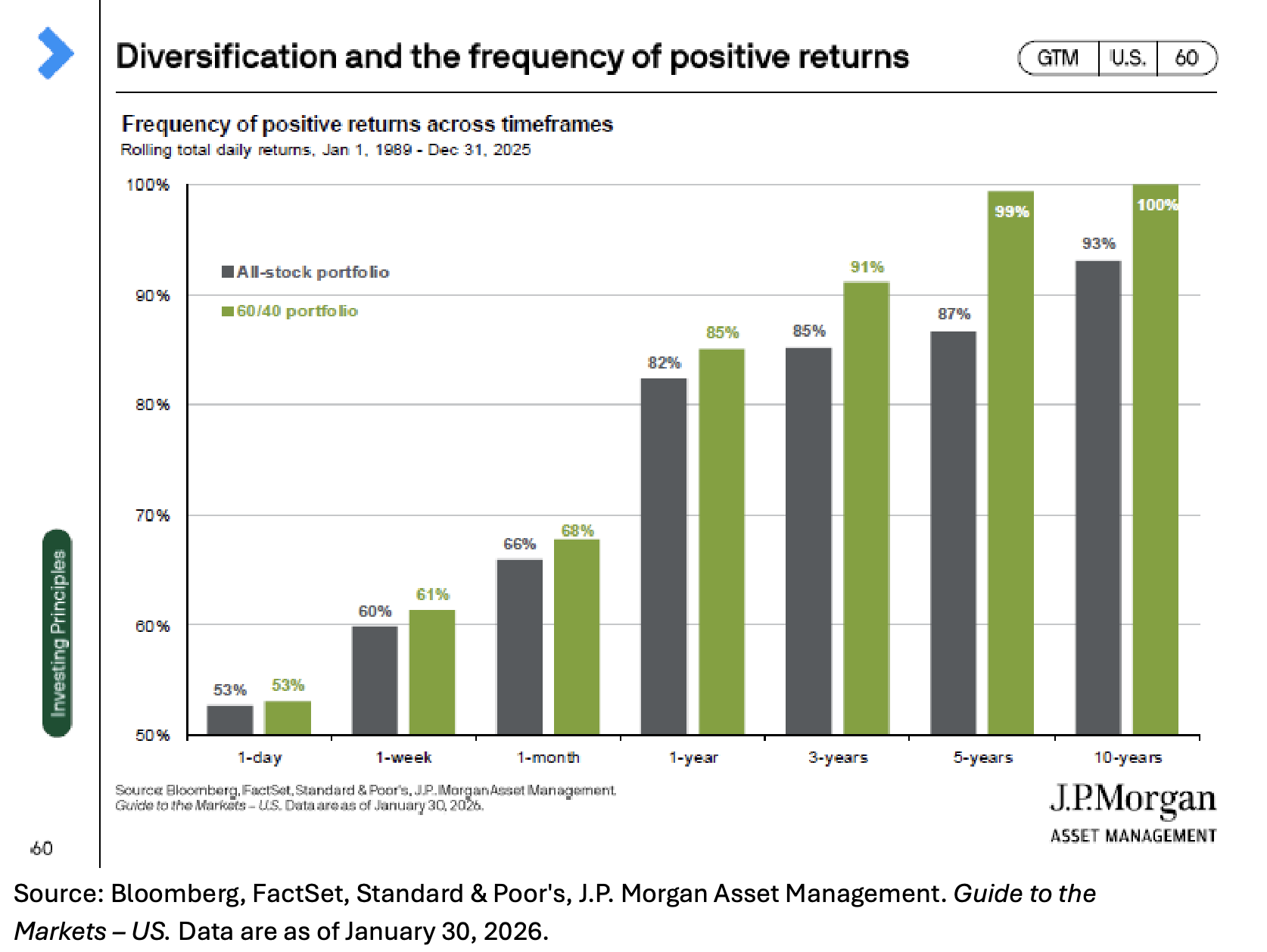

We mentioned in the point above that investment markets go up and down and over time increase. Volatility, or that day to day up and down variability reduces over time. The graph below captures this very well. It is from the JP Morgan Guide to the Markets from January 2026. It looked at data from 1 January 1989 through to 31 December 2025 and shows for both a share only portfolio (grey) and a more balanced portfolio (green), the frequency of positive returns across different time periods.

It shows on the far left that both portfolios had about 53% frequency of positive returns across one day. To invert this, 47% of the time a portfolio will return a negative result on a one-day period. As the time frame extends, the frequency of positive returns increases, and likelihood of negative returns falls away. At the right hand side it shows a balanced portfolio returning positive returns 100% of the time for any rolling 10 year period. Even for a portfolio holding 100% stocks it is positive for 93% of the time on a rolling 10 year time frame across the 36 year period. In short, time reduces volatility and the risk of negative returns.

To address the question of whether it is the right time to invest, having addressed your objectives, and your capacity for loss, with a long time frame it is often better, at least arithmetically, to invest rathe than to wait.

Whilst short term volatility can be unsettling, and media headlines confusing, remain focused on your objectives, and if you are uncertain, get professional advice. Speak with us at Black Swan Capital and we can help you navigate the complexities of the financial world and steer you towards achieving your goals.